The European Union is ahead of the pack, but other regions are catching up. Companies and investors with strong ESG credentials will be poised to ride this wave, making the most of the opportunities it presents, while others will be left behind in the wash. Some may even drown as assets are left stranded.

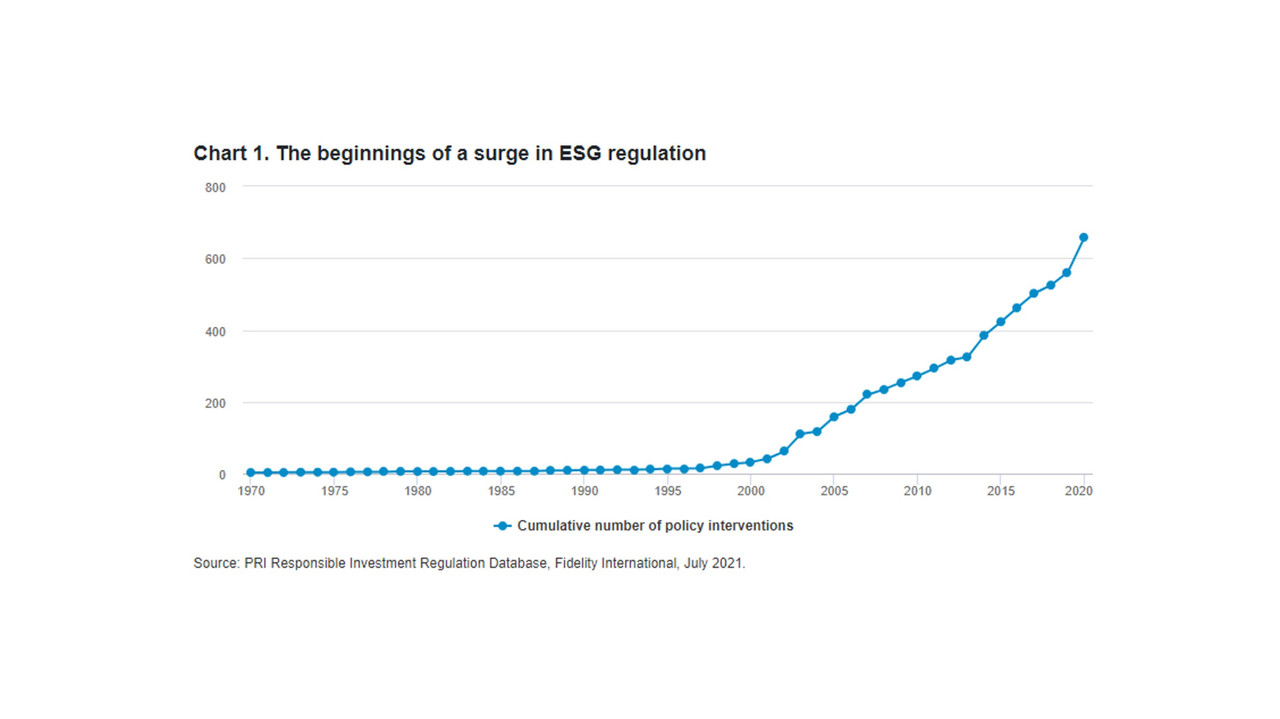

The beginnings of a surge in ESG regulation. (Credit: Fidelity International)

Disclosure is the common thread

ESG data remains a fraught issue. It’s no surprise that regulators are focussed on increasing the quality and consistency of the information available to investors, rather than banning specific investments outright. Investors expect to receive high quality information about a company’s non-financial performance, just as they do for financial performance.

Europe has led the way, creating regulatory blueprints it hopes others will adopt and turn into global ESG standards. By studying what happens there, investors can see what may appear elsewhere. For example, the Taskforce for Climate-Related Financial Disclosures standard is being adopted in several countries around the world, but the EU has its own more stringent climate reporting (the Corporate Sustainability Reporting Directive), that could eventually become the norm.

Current disclosure rules are already beginning to influence investment decisions made by asset managers and companies. This will only increase and ESG will become a decisive factor in attracting funding. Only investment managers who offer high-scoring ESG strategies will attract and retain clients, and it will become harder to justify owning carbon-intensive companies with no plans to clean up their act. Companies without a net zero strategy risk losing investors, suppliers and customers, and being lumped with stranded assets. These forces could alter fund flows and market valuations, and ultimately, accelerate the low-carbon transition.

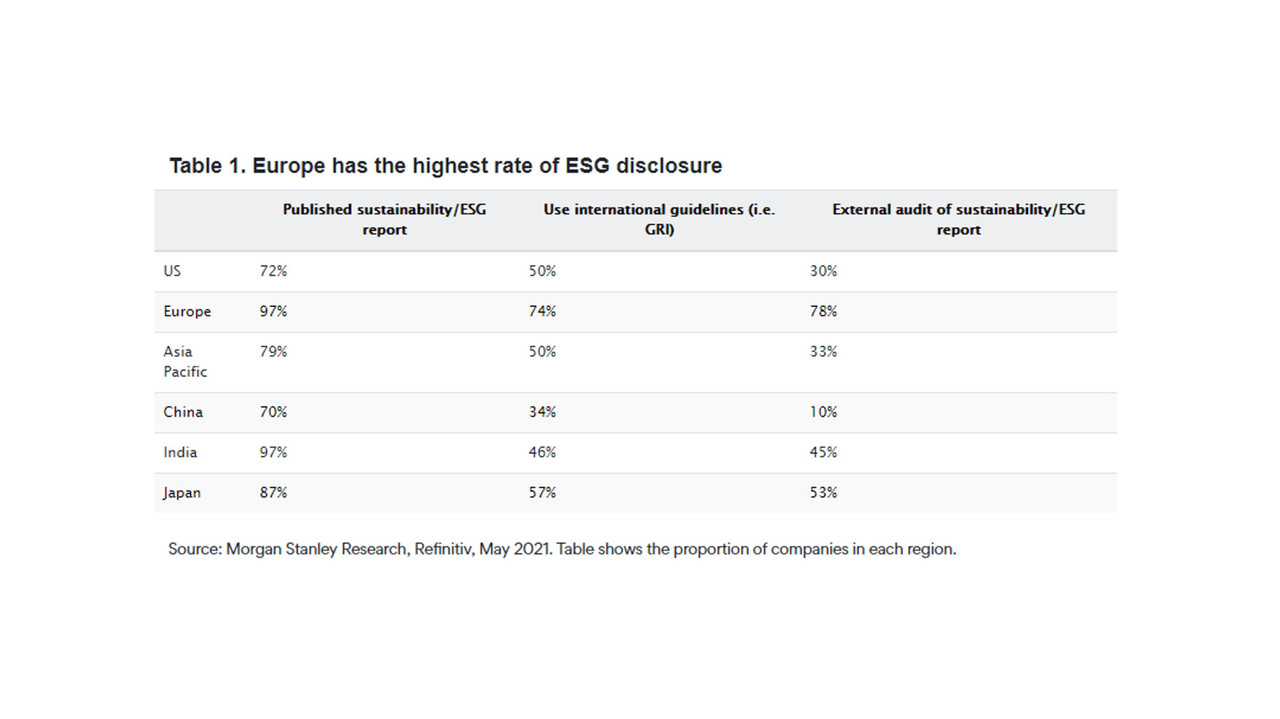

Table 1. Europe has the highest rate of ESG disclosure. (Credit: Fidelity International)

Ensuring investments are sustainable, Europe may have a reputation for sometimes being overly bureaucratic, but its sharp focus on ESG has made it a world leader on sustainability, with the highest climate-related disclosure rates. It has designed a green taxonomy to establish what is and is not a sustainable investment, and – building on this – it has created the Sustainable Finance Disclosure Regulation (SFDR), which aims to limit greenwashing by increasing transparency for investors.

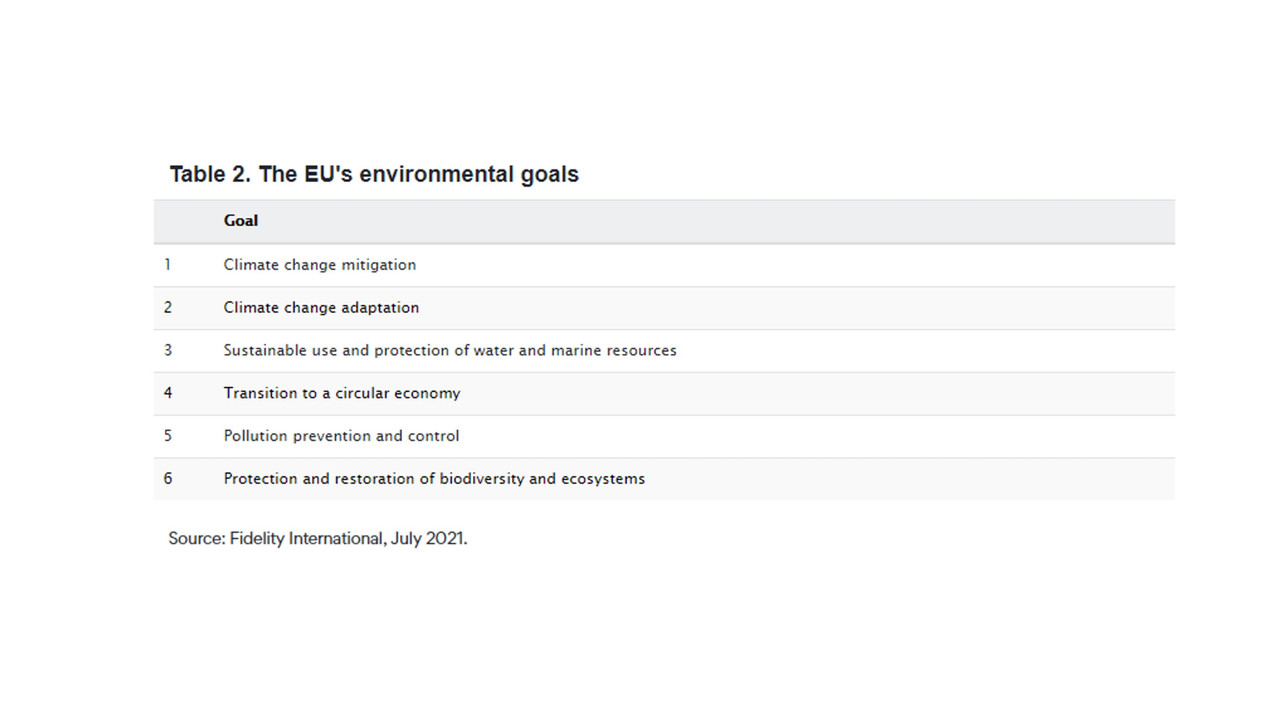

To date, the green taxonomy only covers the first two of the EU’s six environmental goals listed below, but it is expected that future taxonomies will cover the remaining four climate goals, plus additional social goals. The taxonomy includes a reference to the UN Human Rights Charter and International Labour Organisation labour rights (its core principles), so investments that wish to be labelled as sustainable must also meet these social benchmarks.

Table 2. The EU’s environmental goals. (Credit: Fidelity International)

SFDR requires asset managers to disclose how they incorporate sustainability factors into their investment process at a general and fund specific level, using the taxonomy. Funds must be put into four separate bands – Article 6, Article 8, Article 9 and non-ESG – so investors know what level of sustainability they are getting. Article 6 funds must consider sustainability risks as a minimum. However, only Article 8 and 9 funds qualify as ESG-labelled funds, either by integrating sustainability factors into the investment process or by demonstrating a sustainable impact. They must report their alignment with the two climate goals, and not invest in companies that “do significant harm”, though it is not yet clear what significant harm means.

So far, this regulation only affects EU-listed firms and those with EU-based operations, which will have to report their alignment as a percentage of revenues, capital expenditure and operating expenditure. However, the EU is encouraging global convergence through its International Platform on Sustainable Finance, which already includes large Asian countries such as China and India.

Regulatory wave will soon sort winners from losers

With the fight against climate change becoming more urgent by the day, we are in the foothills of a period of global regulatory change that is likely to accelerate. This could revolutionise the way investment portfolios are managed and how companies invest. Well-managed companies with strong risk management have often outperformed during such turbulent periods, but the bias towards quality, good risk management and green growth prospects will be even stronger through this far reaching economic transition; winners and losers will become increasingly apparent over a much shorter timeframe than in the past.