Until recently, only the megabanks continued to build and employ hundreds or even thousands of IT staff to develop and maintain proprietary software. Even some of those are now realising it no longer makes sense. Everyone else, pretty much, had already adopted the model of buying packaged software solutions.

However, the recent rise of the fintechs seems to have reopened the debate, or at least confused the accepted thinking. Suddenly, the world is full of fintech start-ups that attempt to offer innovative financial services that are either digitally delivered or built upon digital concepts such as DLT or blockchain technology.

Even the likes of the “Big Four” consulting firms have published white papers recently highlighting, for those who have perhaps forgotten, or are too young to remember, why buying is better than building.

Perhaps a key reason, or prime source of confusion, lies in the use of the word “fintech” to describe almost any start-up company that combines financial services and technology. The most recent fintech map published by the Luxembourg House Of Financial Technology is a good example, which can be found .

Providers of services including payments, insurance, funds, investments and lending are mixed together with companies that provide the technology platforms and services that underpin the delivery of those financial services. But these are two very different beasts (potential unicorns). The former has a business model and revenue stream based on selling financial services, either in B2C or B2B mode. The latter has a business model based on generating revenue through selling technology, possibly as a service, generally in a B2B model.

The build versus buy equation differs significantly depending on which of these business models is involved. In the former scenario, let us imagine a start-up that is looking to offer existing investment vehicles to a new customer segment through the adoption of new technology, e.g. tokenisation, that creates a new market place. Here, the revenue model is based on attracting investment vehicles onto the platform for distribution to the newly created marketplace of consumers, who also pay something for the convenience of access.

In this case, the core technology is purely a means to an end; it is not the product or service that the fintech will resell to others in order to generate income. User experience and time to market are probably the biggest factors that will determine whether the fintech will see a return on investment – the longer it takes to start generating revenue, the deeper their pockets will need to be and the greater the risk of failure. The perceived high costs of; licensing the software, implementation and maintenance of the system at its core, is actually significantly lower than the eventual costs of building from scratch.

Building a core platform has many clear costs and risks, but also a number of hidden ones, including but not limited to:

· Finding, recruiting and retaining the right IT resources for design, development, testing, production operations, help and support, ongoing maintenance, etc.;

· Time to market, i.e. delaying revenue or even missing market share opportunities, as building takes far longer than deploying an already proven system;

· Immaturity of the solution leading to instability of the platform eventually developed; in addition, making changes required by the market, customers or regulators may become incrementally more expensive over time, as the cost cannot shared (in the same way as it is with a package solution) and the flexibility was not inherently built into the system architecture;

· Less scope for innovation in terms of user experience and use of new concepts, such as tokenisation; such innovation is easier, less costly and lower risk when the core functionality is provided within the solid foundations of a well-established package that adopts a modern architecture offering; cloud deployment, open APIs and functional flexibility that allows new products and services to be introduced quickly and easily without the need for coding.

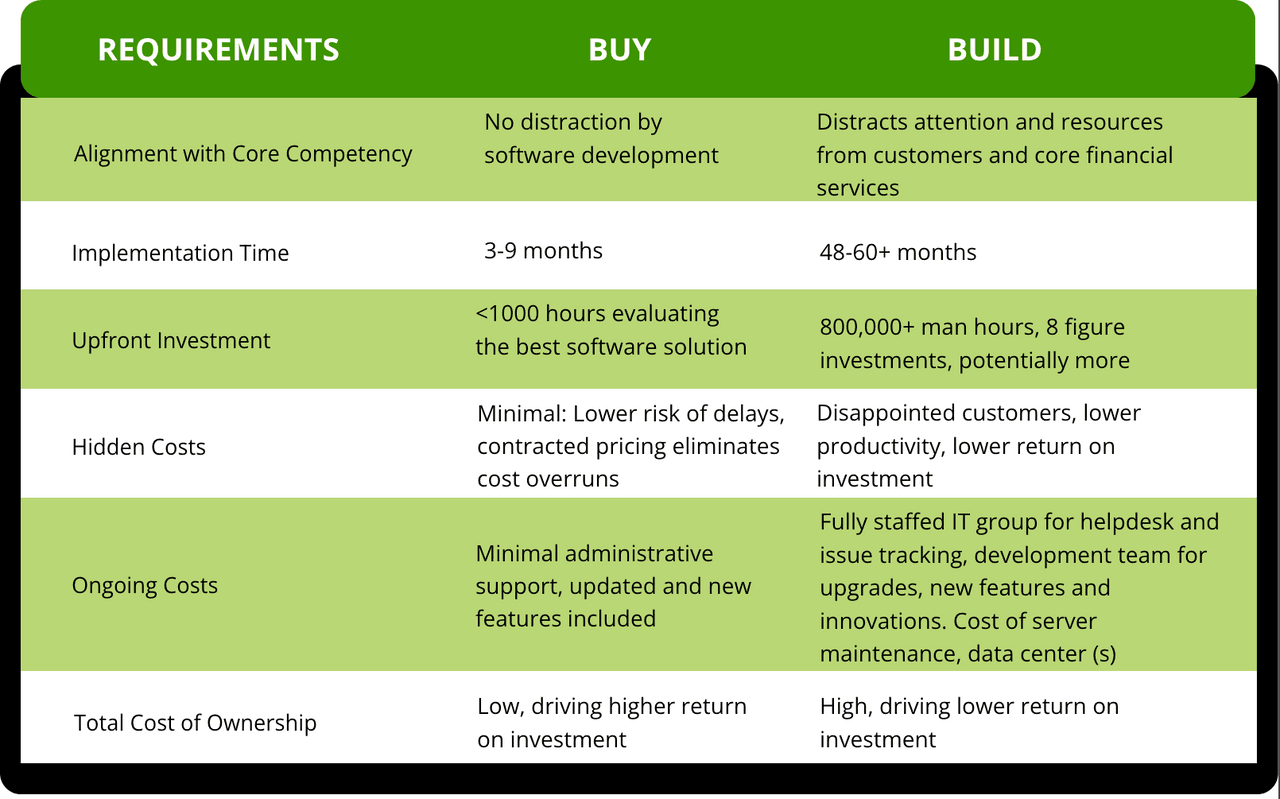

The following table is borrowed from a recent paper published by Deloitte:

To Buy or To Build: Which is the Best Path for Digital Transformation? October 2021 nCino and Deloitte

While some of the estimates in the build column may be considered as being on the high side, the message is, nevertheless, very clear. If you are a fintech, or indeed any financial services provider, then BUY the core systems needed and, if necessary, BUILD the added-value bespoke elements around the core that will differentiate the proposition. The arguments and logic, that have been true for decades, are still just as valid today.

Alan Goodrich

Regional Sales Manager at ERI

ERI is the supplier of the , offering award-winning levels of innovation, real-time process automation and compliance.